A Geopolitical Oil Shock: Between Escalation Risk And Tactical Opportunity

Brent surged 64% in March as Hormuz tensions mount. Explore how geopolitical risks, futures signals, and post-conflict positioning are reshaping oil markets in 2026.

Oil markets have entered a phase of extreme tension. In March, Brent crude futures surged by 64%, one of the strongest monthly performances since 1988, according to LSEG data. West Texas Intermediate followed with a gain of roughly 52%, its sharpest rise since May 2020. So far in April, prices are up more than 7%. This repricing has been driven primarily by disruptions around the Strait of Hormuz, a strategic chokepoint through which close to one fifth of global crude supply transits.

The conflict has now extended into its sixth week, and markets have become increasingly used to political signaling. Recent statements by Donald Trump mark a clear escalation in rhetoric toward Iran, including explicit threats targeting infrastructure and regime stability. “A whole civilization will die tonight, never to be brought back again. I don’t want that to happen, but it probably will,” Trump wrote on Truth Social.

While such communication has heightened uncertainty regarding supply continuity, investors seem to be tempering their fears of a worst-case scenario. Some are betting that despite his bellicose rhetoric, Trump may again extend the 8 p.m. ET deadline for reopening the Strait of Hormuz, as he has already done over the past month. Against this backdrop, is the current oil rally a tactical, volatility-driven opportunity, or a systemic risk necessitating a defensive stance?

volatility As A Trading Environment, Risk As A Portfolio Constraint

For short-term traders, current conditions offer a high-frequency opportunity set. Intraday price swings in both Brent and WTI have widened significantly, creating multiple entry and exit points. However, this environment requires disciplined execution, strict risk controls, and a clear understanding of event-driven price action.

For longer-term investors, the picture is more complex. Since the beginning of the year, oil prices have climbed by more than 80%, briefly exceeding the $120 threshold, a level last observed in 2022. Expectations have already been revised sharply. A recent Reuters poll indicates that analysts now forecast Brent prices to average $82.85 in 2026, compared with $63.85 just one month earlier. This represents a $19 upward revision, or approximately 30%, the largest adjustment recorded since the survey began in 2005. This shift highlights how rapidly geopolitical risk can be repriced into long-term expectations.

Beyond direct military tensions, structural pressures are reinforcing the upward bias. Maritime rerouting, higher insurance costs, and logistical bottlenecks are constraining supply chains. These factors extend the impact of the conflict beyond immediate disruptions and contribute to a sustained risk premium in oil prices. In this context, insufficient or poorly calibrated exposure to energy markets can materially affect overall portfolio performance.

Futures Market Signals: Temporary Shock Or Structural Shift?

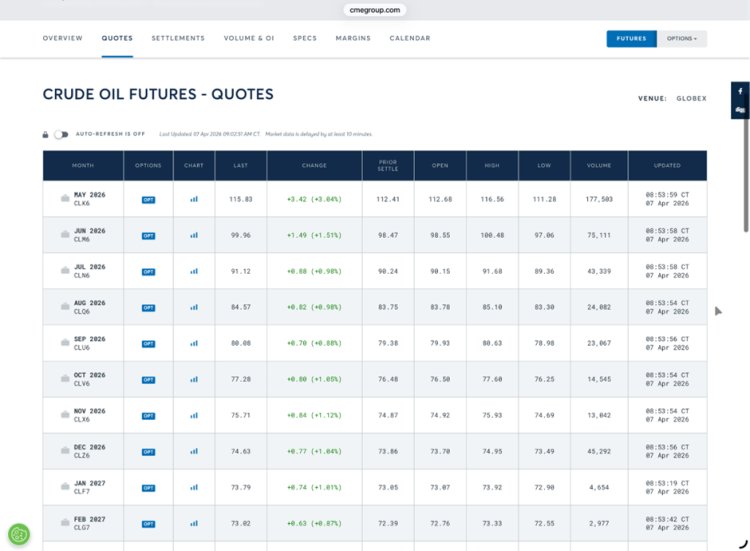

The structure of oil futures provides critical insight into market expectations. Under normal conditions, oil markets tend to operate in contango, where longer-dated contracts trade above spot prices, reflecting storage and financing costs. The current environment, however, is characterized by backwardation, where near-term prices exceed those of longer maturities.

This configuration typically Signals immediate supply tightness combined with expectations of future normalization. In other words, the market is treating the current disruption as temporary rather than structural. If participants were pricing in a prolonged supply deficit, longer-dated contracts would trade at a premium to reflect sustained scarcity.

That said, this interpretation may underestimate operational realities. Even in the event of a ceasefire, restoring damaged infrastructure and normalizing logistics could take significant time. This lag creates a potential disconnect between market expectations and physical market constraints, leaving room for further price reassessment.

According to Indrani De, Head of Research at FTSE Russell, while the market anticipates a gradual easing of prices, it continues to embed a substantial geopolitical risk premium. This suggests that current pricing reflects a balance between expected normalization and persistent uncertainty.

Recent market behavior reinforces this ambiguity. Oil futures have continued to rise following U.S. strikes on Iranian-linked infrastructure, including targets near Kharg Island, ahead of the deadline imposed by Donald Trump regarding the reopening of the Strait of Hormuz. Market commentary from Ritterbusch & Associates indicates that prices appear to reflect either expectations of delayed escalation or the possibility of a negotiated outcome. A direct attack on Iran’s energy infrastructure would represent a significant escalation, potentially triggering a new leg higher in prices.

Post-Conflict Positioning: Where Could Opportunities Emerge?

If the current shock proves temporary, the end of the conflict will likely trigger a reallocation of capital across regions and asset classes. Logically, assets most heavily penalized during periods of geopolitical stress tend to exhibit the strongest rebound once conditions stabilize.

European and Asian markets are particularly exposed. Their structural dependence on energy imports and proximity to Middle Eastern trade flows have made them more vulnerable to recent disruptions, resulting in notable corrections. This positioning implies a higher sensitivity to any improvement in the geopolitical outlook. In contrast, U.S. markets have demonstrated relative resilience. Greater energy independence and the safe-haven status of the dollar have supported capital inflows.

This divergence suggests that, in a normalization scenario, European and certain emerging markets could offer stronger recovery potential through a catch-up effect. However, this outcome is contingent on a credible and sustained de-escalation. According to JP Morgan, ongoing risks to Gulf infrastructure or the possibility of targeted attacks could delay any meaningful normalization and prolong volatility across global markets.

Sources: The Wall Street Journal, CNBC, Reuters, CME Group, LSEG, The Financial Times, BBC

What's Your Reaction?